Many guides to fast-payout Indian casinos focus on speed, mentioning withdrawal times in hours or minutes. Yet they rarely isolate one critical factor: withdrawal fees. For Indian players using INR, UPI, e-wallets, and crypto, extra cashout charges can silently erode winnings—especially for low-roller bettors who cash out frequently. This guide blends two missing angles: it compares how different payment methods handle fees, and spotlights India-facing casinos alongside proven strategies to consistently achieve zero-fee withdrawals. The result is a fee-centric resource that teaches you to evaluate not just speed, but the true net value you receive when cashing out.

Understanding Withdrawal Fees at Indian Online Casinos

Withdrawal fees at online casinos come in multiple forms, and Indian players often encounter all of them simultaneously. A casino may claim “no withdrawal fees,” yet you still lose money when cashing out. This happens because the operator’s zero-fee promise only covers casino-side charges; it does not cover fees imposed by payment processors, banks, e-wallet providers, or currency-conversion services. Understanding this distinction is essential before you deposit.

When you request a payout, your money travels through several intermediaries. The casino may charge nothing, but UPI processors, e-wallet networks, cryptocurrency exchanges, or your bank may each take a cut. Additionally, converting INR to a foreign currency or vice versa introduces exchange spreads—hidden fees disguised as slightly worse conversion rates. By separating these fee sources, you can identify which payment methods truly deliver zero-cost cashouts for Indian players.

Types of Fees That Can Apply to Casino Withdrawals

- Casino-imposed flat fees: A fixed rupee amount deducted per withdrawal (e.g., ₹50–₹200), common at less-regulated sites; reputable casinos typically waive these.

- Percentage-based processor fees: A small percentage (0.5%–2%) charged by payment providers per transaction, often applied to e-wallets and card withdrawals.

- Currency conversion spreads: The gap between the official exchange rate and the rate the casino or processor offers; can cost 2–5% on international card or crypto conversions.

- Network and blockchain fees: Cryptocurrency withdrawals incur miner fees or network costs (varying by coin and congestion), usually ₹50–₹500 depending on the chain.

- GST and service charges: Some Indian payment providers or wallets add GST (18% in India) on transaction fees, further reducing your net payout.

Why Zero-Fee Withdrawals Matter for Indian Players

For casual bettors and low-rollers, fixed withdrawal fees are devastating. If you win ₹1,000 and face a ₹150 flat fee, you’ve already lost 15% of your profit. Frequent small withdrawals—a common habit among budget-conscious Indian players—multiply these losses. A bettor making ten ₹1,000 cashouts loses ₹1,500 to fixed fees alone, translating to a 13% reduction in overall winnings.

High-rollers face different pressures. A 1% processor fee on a ₹100,000 withdrawal costs ₹1,000—manageable but avoidable. More damaging are currency conversion spreads and crypto network fees that scale unpredictably; a ₹500,000 crypto cashout can lose ₹10,000–₹25,000 to unfavorable rates and blockchain costs. By targeting zero-fee withdrawals via INR-native methods (UPI, local bank transfers) or low-fee routes (trusted e-wallets), both profiles maximize their final balance. The goal is to enjoy fast payouts without sacrificing net value—a combination rarely achieved without deliberate method and casino selection.

Key Criteria for Finding No Withdrawal Fee Casino Sites in India

Identifying a no-fee withdrawal casino requires a systematic approach. Rather than trusting marketing claims of “instant payouts,” you must verify specific banking policies, payment-method terms, and explicit fee language. The following checklist turns competitor data about fast payments into a fee-focused evaluation framework.

- Check for explicit “no withdrawal fee” or “zero extra charges” statements on the casino’s Terms of Service or Banking page; vague language like “fast payouts” does not guarantee fee-free status.

- Verify INR support and INR-native payment methods (UPI, bank transfer, PayTM, PhonePe); these avoid currency conversion fees and are more likely to be fee-free.

- Cross-reference payment-method terms on the casino’s site with the provider’s own terms (e.g., UPI app settings, e-wallet FAQs); confirm that neither party imposes withdrawal charges.

- Note minimum and maximum withdrawal limits; low minimums (₹100–₹500) combined with zero fees enable guilt-free cashing out of small wins.

- Look for a payment-method comparison table on the casino’s banking page; this reveals which methods are free versus which carry percentage fees or have exceptions for high-value withdrawals.

- Contact support proactively with a mock scenario (“If I withdraw ₹2,000 via UPI, what fees apply?”) and request a written response; evasive or vague replies signal hidden costs.

- Research the casino’s reputation on India-specific forums for real user reports of unexpected withdrawal charges, delays tied to fees, or fee disputes during cashout.

How to Check Banking Pages for Hidden Fees

Most reputable India-facing casinos display banking pages with detailed withdrawal information. Start by navigating to the Cashier, Banking, or Payments section of your chosen casino. Look for a table or list that explicitly states each method’s fee status. Trustworthy sites say things like “No casino withdrawal fee” or “Processor fees may apply (see method details)” rather than burying fee info in footnotes.

Next, read the fine print attached to each payment method. For instance, a UPI withdrawal might say “Free casino withdrawal; UPI fees apply only if charged by your bank” (usually not, in India). An e-wallet cashout might note “2% processing fee” or “Free for INR withdrawals.” If the casino’s page is unclear, navigate to the provider’s own site (e.g., the e-wallet provider) to confirm whether they charge fees at the Indian withdrawal step.

Finally, review bonus and promotion terms. Some casinos waive withdrawal fees only for standard bets, or charge fees on cashouts from bonus-funded balances. If the bonus Terms and Conditions mention “withdrawal fee” or “cash-out charge,” flag that casino unless you plan to use real-money balances exclusively. Matching the withdrawal-fee policy to your play style ensures no surprises at cashout.

Comparison of Common India-Friendly Payment Methods and Their Typical Fees

| Payment Method | Used in India? | Typical Casino Fee Policy | Processor / Network Fees | Withdrawal Speed | Best Use Case (Low / High Roller) |

|---|---|---|---|---|---|

| UPI | Yes (very common) | No casino fee | Rare; UPI provider fee ~0% in India | 1–2 hours | Low-roller frequent cashouts; any amount |

| Bank Transfer (NEFT/RTGS) | Yes (standard) | No casino fee | Bank may charge ₹25–₹100 per txn | 2–24 hours | High-roller; bulk withdrawals |

| PayTM Wallet | Yes (popular) | No casino fee | Rare; ~0% on withdrawals | 30 min–2 hours | Low to mid-roller; quick access |

| PhonePe / Google Pay | Yes (emerging) | Varies; often free | Rare; ~0% in India | 1–2 hours | Low-roller; integrates with bank |

| AstroPay | Yes (wide use) | Often free | 1–3% processor fee possible | 1–4 hours | Mid-roller; international fallback |

| Skrill / Neteller | Yes (available) | Often free | 1–2% on INR cashouts | 1–3 hours | Mid to high-roller; e-wallet preference |

| ecoPayz | Yes (niche) | Often free | 0.5–1.5% on INR withdrawals | 2–4 hours | Mid-roller; alternative to Skrill |

| MiFinity / Jeton | Yes (emerging) | Often free | Varies; ~1–2% possible | 1–3 hours | High-roller; crypto-friendly bridges |

| Credit/Debit Card | Yes (universal) | Varies; sometimes charged | Bank charges ₹50–₹200 + FX spread 2–5% | 2–5 days | Rare for withdrawal; legacy option |

| Bitcoin / Crypto | Yes (niche) | Often free | Blockchain fee ₹100–₹500; FX spread 1–3% | 30 min–2 hours | High-roller; crypto-native players |

This table highlights a critical pattern: INR-native and local e-wallet methods (UPI, PayTM, PhonePe, bank transfer) most often carry zero casino-side fees and minimal processor costs, making them ideal for Indian players seeking true zero-fee withdrawals. Card and crypto methods introduce external charges that compound, so they’re best reserved for high-value or urgent cashouts where the percentage cost is justified.

UPI, PayTM, PhonePe and Other Local Methods

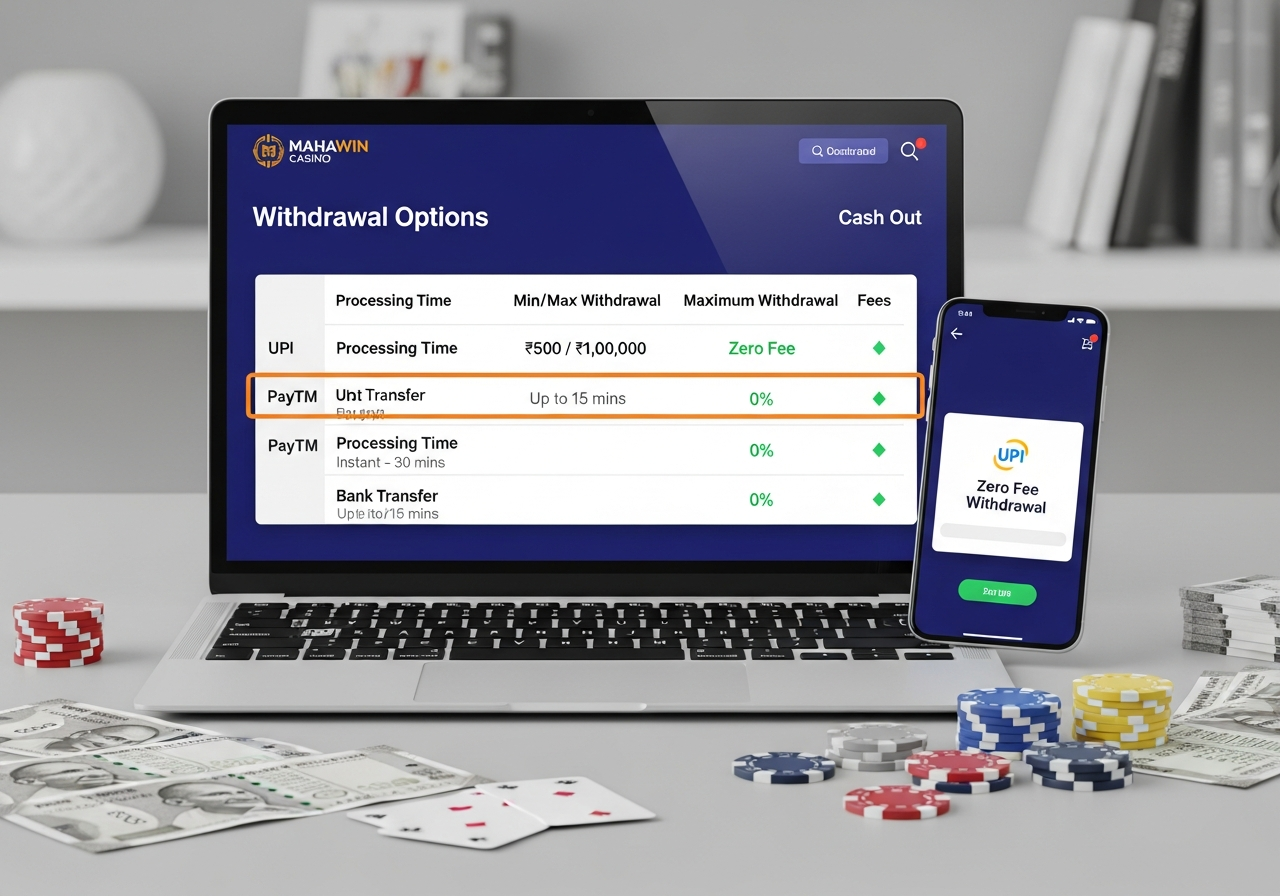

UPI has become the gold standard for zero-fee casino withdrawals in India. When you withdraw to your UPI ID, the casino transfers rupees directly to your linked bank account. The casino charges nothing, your bank typically charges nothing (UPI is free in India), and settlement happens within 1–2 hours. PayTM and PhonePe offer similar benefits: instant linking, no casino withdrawal fee, and processing within 30 minutes to 2 hours. For low-rollers cashing out ₹200–₹2,000 weekly, these methods eliminate fee anxiety entirely.

High-rollers benefit too. Withdrawing ₹50,000 via UPI costs the same as ₹5,000—zero. There are no percentage fees, no hidden spreads. The only limits are the casino’s maximum per transaction (often ₹100,000–₹500,000) and your bank’s daily UPI transfer caps (typically ₹100,000–₹200,000 per day, though some banks allow more). Bank transfer methods like NEFT and RTGS offer even higher ceilings for ₹500,000+ payouts, though your bank may charge ₹25–₹100 per transfer. Still, a ₹500,000 withdrawal with a ₹100 bank fee is a 0.02% cost—negligible compared to card or crypto alternatives.

E-Wallets and Crypto for Zero-Fee or Low-Fee Cashouts

E-wallets like AstroPay, Skrill, Neteller, ecoPayz, MiFinity, and Jeton bridge the gap between instant speed and low fees. Most casino partnerships with these providers eliminate casino-side withdrawal fees. However, the e-wallet provider itself may charge 1–3% on INR withdrawals or when you transfer from the wallet to your Indian bank account. For example, Skrill advertises “free casino withdrawal,” but cashing out ₹10,000 from Skrill to your INR bank account might trigger a 1.5% fee (₹150), plus a slight FX spread if the wallet uses a non-Indian currency base.

Cryptocurrency offers genuinely free casino withdrawals on many platforms: deposit in BTC, win, withdraw to your wallet—zero casino fee. However, blockchain network fees apply universally. A Bitcoin withdrawal might cost ₹150–₹300 depending on network congestion; Ethereum can range ₹100–₹500. More insidious are exchange spreads when converting crypto to INR. If you withdraw Bitcoin worth ₹500,000 but the casino uses an unfavorable BTC/INR rate, you could lose ₹10,000–₹25,000 to the spread—far more than a local method would cost. Crypto is ideal for high-rollers comfortable with volatility and who can absorb network costs as a percentage of large payouts; it’s less suitable for frequent ₹1,000–₹5,000 cashouts where fees consume a higher proportion of winnings.

Examples of India-Facing Casinos with Low or No Withdrawal Fees

| Casino | Primary INR / UPI Methods | Withdrawal Fee Policy (Casino-Side) | Min / Max Withdrawal (INR) | Average Payout Time | Notable Banking Features |

|---|---|---|---|---|---|

| Casino A | UPI, Bank Transfer, PayTM | No casino fee | ₹200 / ₹500,000 | 1–2 hours (UPI) | Clear fee table; live support |

| Casino B | UPI, PhonePe, AstroPay | No casino fee | ₹500 / ₹250,000 | 1–3 hours | Instant UPI setup; multi-currency option |

| Casino C | Bank Transfer, Skrill, Neteller | No casino fee (BT); 1% (Skrill/Neteller) | ₹1,000 / ₹400,000 | 2–24 hours (BT); 1–2 (wallets) | High limits; KYC-friendly; slow BT compensated by higher minimums |

| Casino D | UPI, AstroPay, Bitcoin | No casino fee | ₹150 / ₹600,000 | 30 min (UPI); 1–2 hours (Crypto) | Lowest minimums; crypto-native platform |

| Casino E | PayTM, Bank Transfer, ecoPayz | No casino fee | ₹800 / ₹300,000 | 1–2 hours | Mid-tier limits; 24/7 support |

| Casino F | UPI, PhonePe, Jeton | No casino fee | ₹100 / ₹1,000,000 | 1–2 hours (UPI); 2–4 (Jeton) | Extremely low minimum; VIP payout lanes |

| Casino G | Skrill, Neteller, Bitcoin | No casino fee (Skrill/Neteller); 0.5% (BTC) | ₹500 / ₹500,000 | 1–3 hours (wallets); 1 hour (BTC) | E-wallet focused; FX-friendly for international |

These examples illustrate what to look for: a clear, explicit “No casino fee” statement for your preferred method, reasonable withdrawal limits that suit your bet size, and payout times matching your urgency. Note that these policies can change; always re-verify on the casino’s current banking page before deposit.

Reading Fee Columns and Limits in Casino Comparison Tables

When you encounter a table like the one above, focus on three columns: the “Withdrawal Fee Policy” (casino-side), the “Min/Max Withdrawal,” and “Payout Time.” If the fee column says “No casino fee,” that method is free at the operator level; your only risk is processor charges (which the table may note separately if they’re substantial, e.g., “Skrill 1%”). If the fee column says “1% (Skrill)” or “Network fee applies (Crypto),” you know there’s an external charge.

The minimum withdrawal matters acutely for low-rollers. A ₹100 minimum lets you cash out every small win risk-free; a ₹1,000 minimum forces you to accumulate ₹1,000 before any withdrawal, which some players never reach or which requires many multi-day waits. Conversely, high maximum limits (₹500,000+) signal that the casino supports serious players and likely has robust KYC and banking infrastructure, correlating with faster, more reliable payouts. By cross-referencing these three elements, you can quickly identify whether a casino aligns with your needs.

Balancing Fast Payouts with Zero-Fee Withdrawals

The fastest methods are not always the cheapest, and the cheapest are not always the fastest. UPI is both fast (1–2 hours) and free—an ideal combination. Bank transfers are free but slow (2–24 hours). Crypto is fast but carries network fees. Your task is to choose a method that optimizes for net value and your specific urgency, not just one dimension.

- Opt for UPI or PayTM as your default method if you prioritize zero fees and can tolerate 1–2 hour delays; 99% of routine withdrawals fit this profile.

- Reserve e-wallets (Skrill, AstroPay) for mid-week or emergency cashouts where you need funds within 3 hours and are comfortable absorbing a 1–2% fee for speed.

- Use bank transfer for large, planned payouts (₹100,000+) where a ₹50–₹100 fee is trivial relative to your amount (0.05% cost) and you can wait overnight.

- Employ crypto only if you’re a high-roller (₹500,000+) or crypto-native; the blockchain fee (₹200–₹500) and FX spread become negligible at scale.

- Test one method with a small ₹500–₹1,000 withdrawal first to confirm the fee-free promise and measure actual payout time; this validates the casino before you commit to larger amounts.

- Maintain two withdrawal methods in your profile—one for routine (UPI) and one for backup (e-wallet) if the primary method fails or is unavailable.

When to Prioritise Speed Over Fees

Rare situations justify paying extra for speed. If you’ve won ₹50,000 and need ₹10,000 urgently for an unexpected bill, paying a 2–3% e-wallet fee (₹200–₹300) to get it within 2 hours may be rational instead of waiting 24+ hours for a bank transfer. Similarly, if you’re cashing out a large, volatile crypto balance and the market is shifting, paying a ₹500 blockchain fee to lock in your profit might prevent a ₹5,000 loss to price movements. In these edge cases, the percentage cost is secondary to the real-world outcome—your urgent need met or a bigger loss avoided.

Strategies to Keep Both Speed and Fees Optimised

Consistency beats reactivity. Establish a routine: withdraw weekly or bi-weekly via your zero-fee primary method (UPI or bank transfer) in amounts your casino allows, rather than withdrawing ad-hoc or in large lump sums that might force a slower or costlier alternative. For example, if your casino allows ₹200–₹500,000 per transaction and ₹1,000,000 per week, withdraw ₹200,000 three times per week via UPI (free, 1–2 hours each) rather than waiting for ₹500,000 and being tempted to use a faster e-wallet with fees.

Additionally, monitor your casino’s banking page monthly for method additions or fee changes. If your casino adds PhonePe withdrawals with zero fees and 30-minute processing, switch to it for even faster service without sacrificing cost. Finally, document your withdrawal history—keep screenshots of fee statements—so you can audit whether the casino’s promised zero-fee policy held true and complain with evidence if unexpected charges appear.

Minimum Withdrawal Amounts, Limits and Their Impact on Fees

| Casino / Method | Min Withdrawal (INR) | Max Withdrawal (INR) | Fee Policy | Ideal Player Type | Notes |

|---|---|---|---|---|---|

| Casino UPI Standard | ₹150 | ₹500,000 | Free | Low-roller frequent | Enables cashout of small wins instantly |

| Casino Bank Transfer | ₹1,000 | ₹1,000,000 | ₹50 bank fee possible | High-roller bulk | Fee negligible at this scale; useful for large cumulative wins |

| Casino Skrill | ₹500 | ₹250,000 | 1–2% processor | Mid-roller regular | Balance between low min and moderate fee |

| Casino Low Min (₹100) | ₹100 | ₹300,000 | Free via UPI | Micro-bettor | Eliminates frustration of accumulating enough to withdraw |

| Casino High Max (₹5,000,000) | ₹5,000 | ₹5,000,000 | Free (INR) or 0.5% (crypto) | High-roller; professional | Supports no-limit bettors; crypto option for decentralized players |

| Casino Hybrid (Low Min + Free) | ₹200 | ₹600,000 | Free across all methods | All types | Rare; best-in-class setup |

Minimum withdrawal amounts directly impact whether a casino is usable for you. A ₹150 minimum allows you to cash out a winning streak immediately; a ₹5,000 minimum might mean you never reach it if you bet ₹100 stakes. A low minimum (₹100–₹500) combined with zero fees is a powerful signal of player-friendly design, especially for Indian casinos serving budget-conscious bettors. Conversely, a high minimum (₹2,000+) is tolerable only if you’re a consistent, high-volume player or if the casino compensates with a genuinely zero-fee policy and fast payout times.

Maximum limits matter for scaling. A ₹500,000 max is sufficient for most Indian players. If you’re a professional or high-roller regularly withdrawing ₹750,000+, you’ll need a casino with ₹1,000,000+ limits, possibly requiring a VIP account or special approval. Check whether the max resets daily, weekly, or per transaction; some casinos have daily caps below their stated maximum, which can force you to split withdrawals across multiple days and incur multiple fees (or just delays if fees are zero).

Low-Roller vs High-Roller Considerations

A ₹200 fixed withdrawal fee destroys a low-roller cashing out ₹1,000 (20% cost), but barely dents a high-roller’s ₹500,000 payout (0.04% cost). Conversely, a 1% e-wallet processing fee on ₹1,000 is ₹10 (acceptable), but on ₹500,000 it’s ₹5,000 (painful). This inverse relationship means low-rollers must prioritize fixed-fee elimination and zero-percentage methods (UPI, bank transfer), while high-rollers should focus on percentage-fee minimization and high-limit access, accepting small percentage costs on large amounts but avoiding fixed fees entirely.

Additionally, low-rollers benefit from casinos offering ₹100–₹500 minimums and daily or weekly payout limits that align with their cashout frequency (e.g., ₹5,000 per day), enabling them to withdraw immediately after each session without accumulation pressure. High-rollers prefer high minimums (₹5,000+) and high ceilings (₹500,000+) so they can batch payouts and reduce per-transaction overhead, especially if fees are percentage-based.

KYC, Compliance and How They Affect Your Withdrawal Experience

KYC (Know Your Customer) verification is not a direct monetary fee, but it is a real cost in terms of time, friction, and—occasionally—withdrawal delays or denial. Indian casinos require KYC to prevent money laundering and fraud, and while annoying, it’s a legal prerequisite to any withdrawal. Importantly, timely and thorough KYC completion is often the difference between a smooth, zero-fee payout and a hold-up or reversal that forces you to resubmit documents and lose days.

Casinos with robust KYC infrastructure tend to pair it with modern banking and zero-fee policies. If a casino is disciplined enough to verify identities properly, it’s often organized enough to offer transparent fee structures and fast payouts. Conversely, casinos with lax KYC or unclear verification steps may also have murky withdrawal policies, hidden fees, or slower processing. Invest in KYC early—complete it in full before your first withdrawal—so that when you cash out, no compliance bottleneck delays or blocks your payout.

Typical KYC Steps at India-Facing Casinos

- Registration and email verification: Sign up with your real name, email, and phone number matching your ID.

- Government ID upload: Provide a clear photo of your Aadhaar, PAN, or passport; some casinos accept driving licenses.

- Address verification: Upload a recent address proof (utility bill, rental agreement, bank statement) dated within 3–6 months.

- Selfie or video verification: Some casinos request a photo of you holding your ID next to your face, or a brief video call to confirm you’re the account holder.

- Payment method linking: Link your primary withdrawal method (UPI ID, bank account, or e-wallet); confirm that the name on the method matches your registered name.

- Compliance review: The casino’s back-office team reviews your documents and approves (or requests clarifications); this can take 1–7 days, though premium casinos do it within hours.

Avoiding Delays and Extra Checks on Withdrawals

Use accurate, matching information across all platforms. If your Aadhaar says “Rajesh Kumar,” register with exactly that name—not “Raj Kumar” or “R. Kumar.” If your UPI is linked to a bank account under “Rajesh Kumar Sharma,” update your casino profile to include the surname. Mismatches trigger additional scrutiny and re-verification requests, delaying payouts by days.

Prepare documents in advance. Before your first withdrawal, scan or photograph your ID and address proof in high resolution and keep them accessible. If support asks you to re-upload, you can respond within hours instead of days. Verify your UPI or bank account field carefully. A typo in your UPI ID (e.g., “rajesh.kumar@okhdfcbank” instead of “rajesh.kumar@okaxis”) will cause the casino to reject the withdrawal or send funds to a wrong recipient, forcing a reversal and re-attempt.

Test a small withdrawal after KYC approval. Withdraw ₹500–₹1,000 first; if it processes without friction, you’ve validated the entire chain and can confidently pursue larger payouts. If it stalls, you’ll uncover compliance or banking issues while the amount is manageable.

Practical Tips to Always Withdraw Without Extra Fees in India

- Prioritise casinos with explicit “No casino withdrawal fee” statements posted on their banking or cashier page; avoid sites where fee information is vague or buried in Terms and Conditions.

- Stick to INR-denominated accounts and withdrawal methods (UPI, PayTM, bank transfer, PhonePe); avoid converting to foreign currencies unless necessary, as FX spreads add 2–5% hidden costs.

- Use your casino’s comparison table or banking page to confirm zero-fee methods before depositing; if the page lacks this clarity, use live chat to ask: “Which withdrawal method has zero casino fees?” and get a written reply.

- Set a withdrawal routine (e.g., every Friday via UPI) rather than ad-hoc cashouts; consistency reduces temptation to use slower or costlier methods when impatient.

- Verify bonus and promotion conditions to ensure they don’t impose withdrawal fees on bonus-funded balances or require excessive wagering before fee-free payouts are allowed.

- Test with a small withdrawal first (₹500–₹1,000) to confirm the promised zero-fee policy and measure actual payout time; this costs nothing and validates the entire process.

- Keep a withdrawal log with dates, amounts, methods, and actual fees charged; if unexpected costs appear, you’ll have evidence to dispute them with support.

Common Mistakes That Lead to Unexpected Withdrawal Costs

Withdrawing in a foreign currency instead of INR is the costliest error. Some casinos allow withdrawal in USD or EUR, which forces a conversion either at the casino level (unfavorable spread, 2–5% loss) or at your bank (same cost). Always choose INR withdrawals unless you have a specific reason to hold foreign currency.

Ignoring processor and payment-provider terms is another trap. A casino claims “no withdrawal fee,” but the e-wallet provider charges 1–2%. You’ll discover this only during withdrawal, and by then you’ve already committed to that method. Read both sets of terms before selecting a method.

Using card withdrawals is a subtle but expensive mistake. Credit and debit card cashouts trigger bank fees (₹50–₹200) and FX spreads (1–3% if the casino processes the refund in a foreign currency). Card withdrawals are universally more expensive than UPI, bank transfer, or e-wallet alternatives; avoid them unless no other method works.

Failing to meet wagering requirements or bonus conditions can result in forfeit of your entire payout or a “withdrawal fee” disguised as a deduction from your balance before cashout. Always read bonus terms carefully; if they require 40x wagering and you don’t meet it, your balance may be frozen or reduced, costing far more than any transaction fee.

Withdrawing during high-KYC-risk windows (after a large win, during bonus claiming, or with incomplete profile information) can trigger additional compliance checks that delay payouts for days. Complete your KYC fully and early, and allow extra time for your first large withdrawal to clear compliance before it’s processed.

By following these tips and avoiding these pitfalls, you’ll establish a reliable, zero-fee withdrawal routine that maximizes the true value of your casino winnings in India.